EVS reports 2025 results

27 Feb 2026 18:30 CET

Issuer

EVS

Publication on February 27, 2026, after market closing

Regulated and inside information

EVS Broadcast Equipment S.A.: Euronext Brussels (EVS.BR), Bloomberg (EVS BB), Reuters (EVSB.BR)

EVS Delivers Fifth Consecutive Year of Record Revenue Results with Accelerated Momentum in North America

EVS was able to deliver growth for the fifth consecutive year in a row, despite 2025 being a year marked by geopolitical and macroeconomic challenges. The strong performance continues to underline our ability to realize base growth, fully in line with our PLAYForward strategy, even in an uneven year without Big Event Rental revenue. We see all of our strategic pillars thriving and especially note the break-through growth in North America following our “double down” strategy in that region. We also strengthened our portfolio with 2 new company acquisitions, forming the new business division T-Motion.

Full-year Highlights

- EVS expanded its portfolio with in the acquisition of two companies forming a new business division T-Motion.

- Revenue comes in at EUR 208.1 million, a growth of 5.1% vs. FY24, at the high-end of our guidance, thanks to strong year-end delivery opportunities and a solid contribution from T-Motion. Normalizing for BER, the growth is of 14.2%.

- Strong gross margin performance, combined with well-controlled operating expenses lead to an EBIT of EUR 43.3 million generating a 20.8% EBIT margin. The EBIT performance lands above the high-end range of our guidance.

- Net profit ends at EUR 38.6 million (18.5% net margin) resulting in fully diluted earnings of EUR 2.73 per share.

- Order intake finishes at EUR 225.0 million, incl. EUR 14.8 million of Big Event Rental (BER), growing 7.8% compared to 2024.

- Net cash position remains strong at EUR 58.4 million despite investments in new acquisitions, share buyback and an increased interim dividend payment in 2025. Our cash base continues providing solid financial power to continue execution of our growth strategy.

Second half Highlights

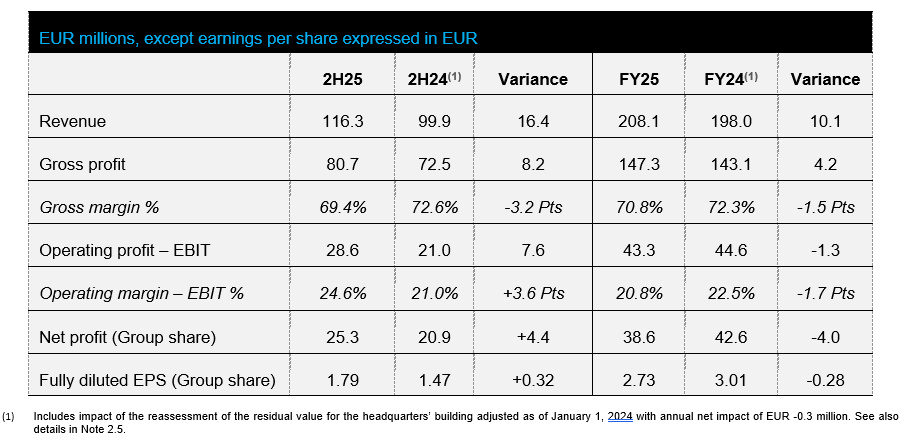

- Revenue for the second half of 2025 ends at EUR 116.3 million, growing 16.4% compared to the same period last year.

- Net profit amounts to EUR 25.3 million, leading to fully diluted earnings of EUR 1.79 per share.

- Strong order intake of EUR 121.0 million with some very large contracts considerably building our long-term order book.

Outlook

The year 2026 starts with a solid order book at EUR 182.2 million, growing 11.3% compared to the same period last year.

The order intake of 2025 strongly contributed to our longer-term order book with some important longer term deliveries scheduled in 2027 and beyond. Next to that, a lot of the fourth quarter order intake contributed to our revenue performance of 2025. This rapid turnaround between order intake and delivery was possible thanks to pre-production activities that have been institutionalized in 2025. Such pre-production allows for shorter delivery terms.

The aforementioned trends impact our order book reserved for 2026, that is estimated at EUR 100.6 million, decreasing -6.0% compared to the officially reported number of EUR 107.0 million at the end of 2024. However, we know that the initial back order base of EUR 107.0 million eroded throughout the year 2025: approximately EUR 10.0 million got moved from 2025 into future periods. We consider this erosion of our 2025 back order as a one-off event, given the adaptations done to our forecasting model throughout the year 2025. The milestones around managed projects are now carefully projected taking into account potential risk factors. As such, we consider a restated order book at the beginning of 2025 of EUR 97.0 million. Post-normalization, we witness an order book that is stronger starting the year 2026 compared to 2025. We acknowledge that this order book includes Big Event Rental revenue.

Our commercial pipeline for 2026 is strong, growing 26% compared to the same period last year, which gives us confidence to see continued base growth in 2026. Next to base growth, we expect full contribution of our new business division T-Motion as well as important Big Event Revenue.

Based on our order book at year-start, our strong pipeline and our ability to optimize production flows, we issue a revenue guidance for the year 2026 between EUR 220-240 million.

From a gross margin perspective we expect to maintain our margins from an organic point of view. The impact of tariffs on the gross profit are expected to be offset by the appropriate price increases. The new business division T-Motion is bound to erode the overall profit margin with approximately 1.0-1.5 points.

From a cost perspective, we will continue to make targeted investments to fuel our growth, primarily by strengthening our teams across the organization to ensure we have the right capabilities and capacity to scale. With the objective of maintaining our operating profit margins, we will carefully balance these investments with our revenue projections.

We expect to pay out dividends for 2025 in line with our dividend policy, namely a base dividend of EUR 1.20 per share.

Key figures

Comments

Serge Van Herck, CEO, comments:

“As we reflect on 2025, I am proud to report another year of strong and consistent performance for EVS. In a media industry undergoing profound transformation, live production has become continuous, multi-platform, and increasingly mission-critical. In this demanding environment, EVS continues to play a central role, trusted by customers worldwide to deliver reliability, efficiency, and operational excellence at scale.

2025 marked our fifth consecutive year of record revenue, confirming the robustness of our business model and the disciplined execution of our PLAYForward strategy. Since 2019, EVS has delivered a compound annual growth rate of more than 12 percent, driven by a balanced mix of organic growth, targeted acquisitions, and sustained customer intimacy.

We once again delivered solid profitability and strong cash generation, supported by operational discipline and the continued expansion of recurring revenue through services, software, and long-term agreements. Our balance sheet remains strong, providing us with strategic flexibility while enabling us to maintain a disciplined capital allocation policy focused on sustainable value creation for our shareholders.

Strategically, we continued our evolution toward a more mission-critical, software-driven company, fully integrated with our high-performance hardware solutions that power the world’s most demanding live production environments. Guided by our PLAYForward strategy, we strengthened workflow integration, deepened customer intimacy, and developed scalable solutions designed for real operational conditions. North America remained a key growth and innovation engine. During the year, we significantly expanded our local organization, further reinforcing our proximity to customers and our ability to scale. Despite tariff-related uncertainties and currency headwinds, we continued to grow rapidly in the region, strengthening our structural position in the world’s largest live production market. In parallel, our continued expansion in the global news market confirms the increasing relevance of EVS technology in 24/7 live environments where speed, accuracy, and resilience are essential.

A defining milestone in 2025 was the creation of the T-Motion division following the acquisitions of Telemetrics (USA) and XD Motion (France). By bringing robotics, automation, and software-defined control together, we expanded our role across the live production chain and strengthened our ability to deliver integrated, intelligent workflows that reduce complexity while enhancing creative flexibility and storytelling.

Innovation at EVS remains firmly driven by real operational needs. In 2025, our R&D teams further advanced software-defined architectures and AI enabled workflows that enhance storytelling, reliability, efficiency, and decision-making in complex live environments. Since 2017, we have invested structurally in Artificial Intelligence and Generative AI, supported today by a dedicated and strategically important team working closely with leading academic and technology partners. Our capabilities are fully embedded in live productions, from XtraMotion delivering super slow-motion on any camera to cinematic enhancement, object tracking, face recognition, intelligent search, automated vertical cropping for social media, and AI-assisted editing tools. All this EVS AI technology can also run “on-premise”, optimizing latency, customer Total Cost of Ownership and carbon footprint. These innovations strengthen our mission-critical value proposition while we continue to embed ESG principles across our operations, reducing product energy consumption and reinforcing responsible supply chain governance.

Partnerships continue to be a cornerstone of our strategy. Our global channel partner ecosystem and technology alliances enable us to scale our impact while remaining focused on our core strengths across sports, news, entertainment, and corporate production environments.

Looking ahead, our ambition remains clear. We are committed to becoming the undisputed reference platform for live production globally, with the long-term objective of scaling toward more than 350 million euro in revenue through sustainable and profitable growth. In 2026, our technology will once again be at the heart of the world’s most demanding live environments, including major global winter sports events and leading international football tournaments. These events reaffirm EVS’s role as mission-critical infrastructure behind the world’s most valuable live moments.

While the geopolitical and macroeconomic environment remains challenging and unstable, we remain cautiously optimistic about the future, confident in the strength of our strategy, our team members, and the trust of our customers and channel partners.

On behalf of the Board of Directors and the entire Leadership Team, I thank our customers, partners, team members, and shareholders for their continued trust and support."

Comments

Commenting on the results and the outlook, Veerle De Wit, CFO, said:

"2025 has been a rewarding year: despite all the geopolitical and macroeconomic challenges, we managed to deliver yet another strong year and secure our continued growth path. All of this whilst delivering a very solid operating margin. The balance has not been easy, and adaptability has been key in 2025, but we can only be happy and proud of the end result.

We delivered a strong order intake at EUR 225 million with some key reference wins and strategic deals. This order intake is coupled with a strong revenue performance at EUR 208.1 million, realizing a 5.1% growth, overcompensating the Big Event Rental revenue of 2024. Our revenue performance has witnessed a different pattern than historically. Both US tariffs and large projects slowed down our revenue recognition pace throughout the year. Towards year-end we were able to accelerate revenue thanks to optimized production flows: pre-production allowed us to be more agile and scalable, enabling to reduce delivery terms and secure deliveries for fourth quarter orders still within the year.

Tariffs also played on our gross profit margins, but with the right price setting, we were able to limit the impact on our overall margin performance.

Finally, our performance was also impacted by a weak dollar throughout the year 2025. At constant currency, revenue would have amounted to EUR 211.6 million, representing a growth at constant currency of 6.9% (delta of 1.8 Pts).

As a company we demonstrated that we can control our spending patterns. After a growth of our discretionary spend of 10.4% in first half, we were able to limit the increase to 3.1% in second half, despite a growing team member base and the integration of new acquisitions. We carefully watched our team member needs and prioritized spend requirements to preserve a solid operating margin of EUR 43.3 million (20.8%). On a constant currency basis related to FY24, the EBIT would have amounted to EUR 46.0 million, corresponding to an EBIT margin of 21.8%.

Our strategy to secure our foreign exchange rate flows (primarily USD and GBP) have allowed us to limit the impacts of a weakening dollar, securing a profit before taxes at EUR 43.1 million. From a tax perspective we realize an effective tax rate of 10.7%, leading to a net profit of EUR 38.6 million (18.5%). It should be noted that the taxes of 2025 include a prior-year catch-up worth EUR 1.2 million. The normalized tax rate, excluding this impact, sits at 7.9% (+1.0 Pts compared to FY24).

From a balance sheet point of view, we see an increase of our receivables, linked to a strong revenue performance in the last month of the year. The total receivables still evolve in line with our turnover. Overall, our balance sheet remains very healthy. With our net cash position at the end of the year of EUR 58.4 million, we continue to have a strong financial power to execute on our PLAYForward growth strategy.

All of the above positions us strongly for future growth and sustained success."

Market & Customers – Sustained Profitable Growth

Strong Presence confirmed at next Major Events

EVS secured a key contract to support a major international football tournament in 2026. As part of this multi‑million‑euro agreement – which will contribute significantly to EVS’s Big Event Rental revenue in 2026 – the company will deliver a comprehensive turnkey solution covering broadcast and media equipment, as well as associated services supporting live replay operations, logging, asset management and file‑based content distribution.

For the first time, the MediaCeption VIA-MAP platform – including fully integrated MediaHub workflows and AI assistance – will optimize the media creative processes during this football tournament. This event will represent a key milestone for EVS in terms of MediaCeption market reference.

Leveraging its latest technologies, including T‑Motion - created following the acquisitions of XD Motion and Telemetrics -EVS has also supported the major winter multi‑sport event, providing advanced robotics, automation and software‑defined control capabilities to enhance the efficiency, reliability and creative flexibility of live production operations.

During the same event, Move Up – a new product developed in 2025 based on the technology acquired from MOG Technologies in 2024 – has also been used within transcoding workflows.

Accelerated momentum in NALA

In 2025, both revenue and order intake in North America continued to accelerate, solidifying the region's role as a strategic growth engine for EVS and validating the company's long-term investment roadmap in the Americas.

EVS signed a significant multi-year agreement worth over USD 15 million with a leading North American media company, substantially boosting order intake. The customer will deploy a comprehensive suite of EVS solutions to modernize production, ingest, and media management workflows, enhancing efficiency, scalability, and long-term infrastructure sustainability for both live and non-live environments. The deal also includes long-term services and support, ensuring reliable, high-performance operations in demanding production contexts.

To support the continued strategic expansion in North America, EVS announced the opening of its new Rocky Mountain Hub in Denver, Colorado. This strategic investment strengthens customer proximity, enhances operational responsiveness, and supports the company's growth across North America's diverse time zones.

To reinforce its regional leadership, EVS appointed Bevan Gibson as Executive Vice President of Sales & Operations for North America. Bevan's extensive industry experience and operational expertise is enhancing EVS's ability to scale its activities, drive commercial execution, and support the expanding customer base across the region.

Revenue and order intake in the NALA region increased significantly (with both order intake and revenue growing 30% year over year in US Dollar), contributing solidly to our overall performance alongside the particularly strong momentum in North America.

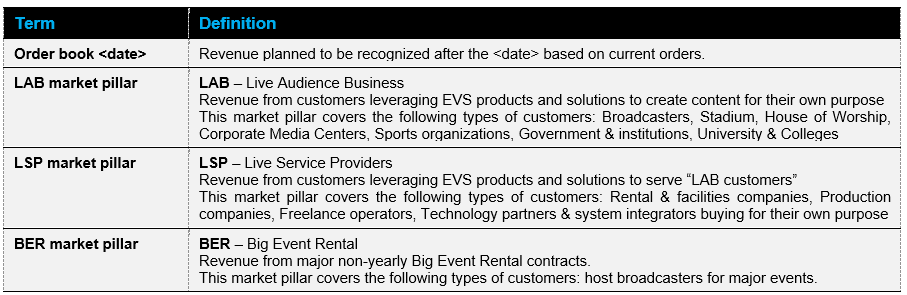

LAB as the market pillar supporting growth, supported by EVS Channel Partners

While the LSP (Live Service Providers) revenue and order intake saw a slight increase, LAB (Live Audience Business) revenue and order intake have continued their significant growth trajectory since 2020.

Live Service Providers are renewing and extending their fleets with XT-VIA servers at the core of the LiveCeption solution, as demonstrated through contracts with FinePoint Broadcast Ltd and Gravity Media. The MediaInfra Cerebrum control system is used as the backbone for managing complex live IP workflows at Gravity Media, while GameCreek, a long-standing customer of the LiveCeption solution, has also selected Neuron View, another MediaInfra product, for its mobile production units. This highlights the value of the EVS ecosystem and the cross-selling between LiveCeption and MediaInfra solutions.

In the LAB market pillar, the MediaCeption VIA-MAP solution continues to expand among large customers aiming to accelerate their transformation. This is evidenced by the NDR contract, where VIA-MAP will be used for “Tagesschau”, a leading news program in Germany. In Belgium, the Royal Belgian Football Association has selected Xeebra to power Belgian football’s centralized VAR operations in collaboration with Gravity Media. Media Infrastructure solutions are increasingly being deployed among LAB customers, extending beyond traditional broadcast players to include stadiums, corporate environments, and houses of worship.

EVS Channel Partners play a crucial role in LAB customer transformation. At IBC, EVS and Qvest announced a strategic partnership to redefine broadcast workflows based on the Flexible Control Room (FCR) solution. Revenue generated by Channel Partners continue to increase at a faster rate than those from direct sales.

Supply Chain Resilience and Operational Readiness

Amid ongoing geopolitical uncertainties, EVS remains proactive in mitigating potential supply chain disruptions and application of US tariffs.

We also remain vigilant to any geopolitical impact that may come in the near future and do proactively define strategies to tackle any change in market conditions.

Technologies

Continued Investment in Technological Innovation

EVS remains steadfast in its commitment to driving innovation within the broadcast and media industry. In line with our strategic objectives, we continue to dedicate over 40% of our workforce to the technological development of our products and solutions. This unwavering focus is fundamental to our ability to stay ahead in a rapidly evolving industry. Our mission is to empower customers and EVS operators with cutting-edge tools that address their most pressing operational challenges.

Advancements in Live Media and Broadcast-Specific Generative AI

EVS and the University of Liège (ULiège) have established the academic chair “Computer Vision and Data Analysis for Sports Understanding,” led by Professor Anthony Cioppa. This initiative aims to develop AI approaches for automatically understanding sports images and videos, marking a significant milestone in the collaboration between academic research and industry.

The marketability of EVS's generative AI technologies is further proven by the new effects in the latest XtraMotion release. Since its debut in 2021, XtraMotion has gained global recognition for creating super slow-motion content from any camera using advanced AI. It has received several industry awards and is trusted by major networks and productions worldwide. The latest release introduces the “deblur effect”, which eliminates motion blur from fast-moving cameras, and the “Cinematic effect”, which simulates shallow depth of field for a film-like aesthetic. These effects, offered under a single license, provide sports broadcasters and media companies with more creative possibilities to enhance the visual impact of key moments during live action.

Innovation Beyond Generative AI

LiveCeption Zoom: Integrated into the LiveCeption® solution family and controlled via LSM-VIA, this feature allows replay operators to zoom into camera feeds using touch gestures, capturing every detail with precision.

Xeebra VAR: Officials benefit from reviewing more camera angles simultaneously, thanks to increased channel density and improved AI-based Video Offside Line.

Move I/O and Move UP: These tools streamline media ingest, playout, and transcoding workflows, enhancing efficiency and flexibility. Developed through collaboration between EVS teams in Liège and Porto, following the acquisition of MOG Technologies in 2024.

Tactiq: Launched at IBC, Tactiq is at the core of the Flexible Control Room solution, transforming media production. It decouples the user interface from backend systems, providing unified control of video, audio, graphics, and lighting in one modular interface. This software-defined approach enhances operational flexibility, allowing any workstation to be assigned any task, operated via touchscreen or physical controller, and maximizing team efficiency.

Commitment to Technological Sustainability

EVS is deeply committed to sustainability, integrating eco-conscious initiatives across all aspects of our business. Reducing power consumption and carbon footprints has become a key focus for our development teams, driving continuous improvements through architectural optimizations, product innovations, and software efficiency enhancements. These efforts reflect our broader responsibility toward environmental stewardship and our commitment to fostering a more sustainable future for the industry.

Corporate topics

Ongoing Transformation and Strategic Growth

EVS continued to evolve in 2025, further aligning its organization and capabilities with the company’s accelerating growth trajectory. A major focus this year was scaling our regional presence to support long-term development. In North America, our footprint expanded significantly, with the team growing from around 50 team members at the end of 2024 to more than 100 by the end of 2025, reinforcing our proximity to customers and strengthening execution capacity in the region. In parallel, we continued to invest in our Porto hub, following the 2024 acquisition of MOG Technologies, welcoming new talent and further building this location into a key center of expertise within the group.

Increasing operational excellence remained a key priority throughout the year. Continued investments in internal systems, processes, and digital tooling improved efficiency and collaboration across teams. While many of these enhancements operate behind the scenes, they play a critical role in enabling faster decision-making, greater agility, and a more seamless experience for customers working with EVS.

Strategic Acquisitions & Investments

In October, EVS finalized the acquisition of Telemetrics, a US-based company specializing in indoor Media Production Robotics, as well as XD Motion, a French company that is renowned for its innovative control systems that enable secure outdoor Media Production Robotic experiences and provides reliable control of indoor robotic arm. Both acquisitions support long-term value creation through portfolio expansion: the combination of the 2 acquisitions leads to a new solution for EVS, named T-Motion. It enables EVS to extend its total addressable market, offering a comprehensive range of Media Production Robotics, both indoor and outdoor. This solution will allow EVS to capture the most powerful live video images and emotions.

Commitment to Corporate Sustainability

Sustainability remains high at the top of our agenda. Our nine core corporate sustainability tracks - which include customer and company carbon footprint reduction, talent management, diversity & inclusion, customer experience, local social contribution, cybersecurity, sustainable supply chain, and business ethics - have further refined their action plans to achieve the targets set forward. EVS remains a recognized ESG leader in the industry, consistently receiving positive market feedback for our commitment to sustainability and responsible business practices. Further details on these efforts and initiatives are presented in our annual sustainability report.

Top employer for the 4th year in a row

For the fourth consecutive year, EVS has been recognized as one of Belgium’s Top Employers, reflecting the strength of our HR practices. This distinction reinforces our employer brand and supports our continued ability to attract, develop and retain top talent worldwide in a highly competitive market.

Capital allocation

In line with the capital allocation strategy defined at the end of 2024, EVS has allocated its operational cash to several pillars throughout the year 2025.

We have seen increased funds being allocated to investment activities. We have funded organic growth (like the Double Down North America plan), but have also allocated operational cash to acquisitive growth in 2025. The two acquisitions, Telemetrics and XD Motion have been paid on a cash basis.

Next to investment activities, we have increased the dividend paid in 2025 to 1.20 EUR per share (compared to 1.10 EUR per share in 2024). During the first months of the year, we have also finalized our EUR 10 million share buy-back program that was launched in November 2024.

No further pillars in the capital allocation strategy were launched in 2025, as the operational cash will be preserved to reconstitute our buffer to execute on future M&A activities.

Second half and full-year revenue

In 2H25, revenue reached EUR 116.3 million, representing an increase of EUR 16.4 million or 16.4% compared to 2H24. Neutralizing the 2024 revenue linked to Big Event Rental, the growth is of 31.3%.

At constant currency, revenue increased by 19.6% YoY.

In the second half of the year, excluding Big Event Rental, LSP represented 38% of the revenue (38% in 2H24) while LAB accounted for 62% (62% in 2H24).

For the full year 2025, revenue reached EUR 208.1 million, representing an increase of EUR 10.1 million or 5.1% compared to 2024. Excluding the 2024 Big Event Rental, the growth is of 14.2%.

At constant currency, revenue increased by 6.9% YoY.

Currency fluctuations primarily impact EVS revenue by the EUR/USD conversion, which can have a significant impact on our results even if EUR/USD fluctuations also impact the cost of our US operations and partially our cost of goods sold. Mind that since the integration of Telemetrics, we now also sell in USD in other continents of the world.

Out of the EUR 208.1 million revenue in 2025, EUR 8.6 million relate to financial leasings, compared to EUR 9.6 million in 2024.

Full-year earnings

Consolidated gross margin ends at 70.8% for FY25, compared to 72.3% in FY24 (-1.5 Pts YoY). This decrease is primarily a consequence of the integration of the new business division T-Motion (explaining -0.6 Pts YoY). Acquisitions generally have a lower margin profile when they get integrated in the company. From a long-term perspective we systematically plan to narrow the gap towards the average EVS portfolio. This objective is generally reached through growth, scale, software development and integration into our ecosystem. Next to an integration impact, the drop in gross margin is also partly related to some changes in the organic EVS business model. Following the implementation of tariffs, EUR 2.1 million has been added to our cost base. However, this effect is largely offset by a sales price increase that we announced over summer applicable to North America.

Operating expenses increased by 7.0% YoY driven by the expansion of team members primarily to support our “double down” North America strategy and the accelerate some R&D tracks. The integration of the different acquisitions also add cost to our operating expense base. After a steep increase in the first half, EVS has demonstrated its ability to control the expenses in second half with the objective to secure a strong operating margin for the year.

Overall the EBIT performance was of EUR 43.3 million, generating an EBIT margin of 20.8%. On a constant currency basis, related to FY24, the EBIT would have amounted to EUR 46.0 million, corresponding to an EBIT margin of 21.8%.

The net profit ended at EUR 38.6 million, with income tax expense amounting to EUR 4.6 million for the full year 2025 (compared to EUR 3.1 million in 2024). The effective income tax rate is at 10.6%, which is higher than in previous years. It is to be noted that the taxes in 2025 include a prior-year catch up worth EUR 1.2 million. Correcting for this one-off, the normalized tax rate is of 7.9%.

The net profit leads to a fully diluted earnings per share of EUR 2.73 (versus EUR 3.01 in 2024).

Second half earnings

The gross profit margin in 2H25 reached 69.3% compared to 72.6% in the same period last year. The decrease in second half is mainly linked to the integration of T-Motion in our numbers in the fourth quarter (accounting for 0.8 Pts delta).

Operating expenses grew 3.1% in 2H25 compared to the same period last year, reflecting the efforts to slow down on expenses after a strong growth in 1H25.

The 2H25 operating margin was 24.6% compared to 21.0% in 2H24 primilarly driven by the additional revenue generated in 2H25 and the strong control over expenses.

The Group net profit amounts to EUR 25.3 million in 2H25 compared to EUR 21.1 million in 2H24. Fully diluted earnings per share amounts to EUR 1.79 in 2H25 compared to EUR 1.47 in 2H24.

Balance sheet and cash flow statement

Balance sheet remains solid with net cash position at EUR 58.4 million combined with low debt level (of which EUR 14.5 million related to IFRS 16), resulting in a total equity representing 72% of the total balance sheet as of the end of 2025.

Working capital requirements reaches EUR 102.2 million, an increase of 11.7% compared to the end of 2024, mainly driven by the increase in trade receivables following recent major project sales in NALA Region, strong deliveries in the last months of the year as well as the incorporation of T-Motion customers balances. Working capital represents 49% of sales at year-end 2025 (42% in 2024). Trade payables increase by EUR 4.6 million, whereas inventory levels remain stable.

The increase in goodwill of EUR 8.1 million results from the two business acquisitions in the period. Other intangible assets include the costs for internal development capitalized since 2022 according to IAS38, as well as technology and customers related intangibles acquired as part of the two business acquisitions of the year.

Lands and building mainly include the headquarters in Liège and the right of use for the offices abroad (IFRS16). In 2025, a re-assesment of the residual value for the headquarters building in Liège has resulted in a correction of historical and prospective depreciation expenses (see details in Note 2.5).

Inventories amount to EUR 35.0 million, a slight increase of EUR 0.5 million compared to the beginning of the year with the aim to support the continuous growth of activities. The ratio of inventory vs. sales remains stable at 17% in 2025.

Liabilities include EUR 14.5 million of financial debt (including long term and short-term portion), mainly related to the lease liabilities. Long-term provisions include the provision for technical warranty on EVS products for labor and parts. Other amounts payable mainly represent deferred income and advance payments received from customers on contracts in progress.

Net cash from operating activities amounts to EUR 27.7 million for the full year 2025, compared to EUR 63.9 million in 2024. The decrease is mainly driven by unfavorable variance in working capital requirements compared to the previous year, mainly on trade and other receivables following the increase in activities especially in North America, combined with unfavorable conversion differences linked to the USD weakening in the period. On December 31, 2025, cash and cash equivalents total EUR 72.9 million, compared to EUR 87.8 million at the end of 2024. The decrease is mainly driven by new acquisitions of Telemetrics and XD Motion in the period, share buyback program at the beginning of the year, increased interim dividend payments as well as investments in intangible and tangible assets and reimbursement of lease liabilities, partially offset by the net cash flows from operating activities.

At the end of December 2025, there were 14,327,024 EVS shares outstanding, of which 922,093 were owned by the company with an average purchase price of EUR 23.26. At the same date, 824,395 warrants were outstanding with an average exercise price of EUR 27.38 and maturities between October 2026 and October 2031.

Team members

At the end of 2025, EVS employed 792 full time equivalent team members. This is an increase of 87 FTE compared to the end of 2024 (705 FTE). In 2025, the acquisition of Telemetrics and XD Motion accounted for 37 of these 87 new team members. For 2026, we expect an increase in the number of team members, so as to continue and fuel our future growth.

Corporate update

There has been no further change to the composition of the Board of Directors since the last General Assembly on May 20th 2025 during which the shareholders have renewed the mandate of Chantal De Vrieze, independent director (representing 7 Capital bv) for a period of 4 years. The Board of Directors is currently composed of nine directors:

Johan Deschuyffeleer, independent director & President (representing The House of Value BV);

Michel Counson, managing director;

Martin De Prycker, independent director (representing InnoConsult BV);

Chantal De Vrieze, independent director (representing 7 Capital SRL);

Frédéric Vincent, independent director;

Marco Miserez, independent director;

Anne Cambier, independent director (representing Accompany You SRL);

Serge Van Herck, CEO and managing director (representing InnoVision BV) ; and

Soumya Chandramouli, independent director (representing FRINSO SRL).

Glossary

In case of discrepancies between the English and the French Version, the English Version prevails.

Conference call

EVS will hold a conference call in English on March 2nd 2026 at 9.00 am CET for financial analysts and institutional investors. Other interested parties may join the call in a listen-only mode. The presentation used during the conference call will be available shortly before the call on the EVS website.

Participants must register using the following link: register here

Corporate Calendar

- May 19th, 2026 : general assembly

- May 21st, 2026 : 1Q 2026 business update (post market publication)

- August 18th, 2026 : 2Q 2026 and 1H 2026 results (post market publication)

- November 17th, 2026 : 3Q 2026 business update (post market publication)

Source

EVS

Provider

Presspage

Company Name

EVS BROADC.EQUIPM.

ISIN

BE0003820371

Symbol

EVS

Market

Euronext